By the numbers: the Facebook prospectus

Facebook's IPO has been compared to Google as the next big opportunity to invest in a massive internet enterprise, but how much is hype and how much is realistic?

One thousand dollars of Google shares from 2004 would be worth about $6000 today. Not bad, considering we've been through a period of economic turbulence. So you can understand the enthusiasm to jump into Facebook, the online phenomenon that could give Google a run for its money.

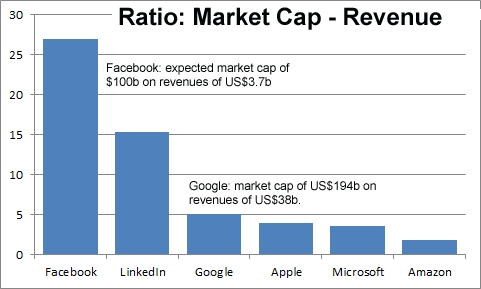

It's a long bow, though, isn't it? Google is a US$193 billion company with revenues of US$38 billion. Facebook has one 10th of Google's revenue, yet it's expected that after listing it'll be worth half as much as Google. As the graph shows, a market valuation 27 times revenue (or 102 times earnings) is out of kilter with comparable tech stocks — and, really, out of kilter with common sense.

(Credit: Phil Dobbie/ZDNet Australia)

The Facebook Prospectus, released on the weekend, does little to argue the case for this enormous discrepancy. Revenue, it says, will come from advertising and payments. Facebook says its combination of "reach, relevance, social context and engagement" will drive up ad revenue. Yet, the nature of the site could make this difficult. Does advertising blend as smoothly into a social-networking environment as it does into a search situation? That might be why the prospectus says, "We believe that most advertisers are still learning and experimenting with the best ways to leverage Facebook to create more social and valuable ads".

There's less hype around Facebook's second revenue opportunity: online payments. That will, surely, only ever be a small slice of its pie. The prospectus points to an "industry source" putting this market at US$15 billion by 2014. Facebook will only get a share of that if it's in response to advertising on the site, which really makes its revenue a single-stream strategy. Risks are also noted in the prospectus: "The loss of advertisers, or reduction in spending by advertisers with Facebook, could seriously harm our business."

That major risk aside, we can expect some hype at the onset. The price is built on the opportunity rather than where the company is now. When Google listed in 2004, the company was worth US$23 billion, 218 times earnings. I'd argue, though, that it went to market with a clearer idea of how it was going to make money. Still, if Facebook sees the same growth rate as Google, we could be seeing a $600 billion company by the end of the decade. Is it worth the punt?