Softbank as Sprint's savior: What $20.1 billion does, doesn't do

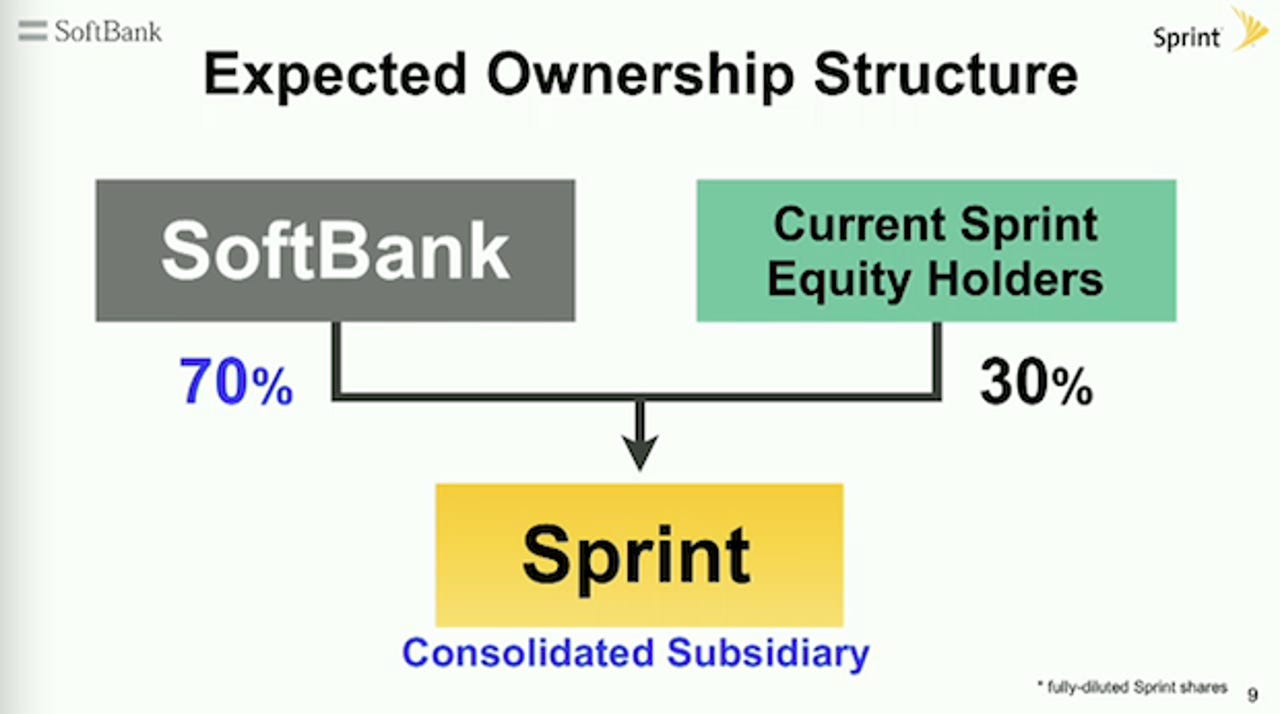

Softbank officially bought 70 percent of Sprint, which diluted its shareholders to bolster its balance sheet, and essentially saved the wireless carrier. But this Softbank investment isn't perfect and Sprint still has numerous challenges ahead.

The deal breaks down like this:

- Softbank will invest $20.1 billion in Sprint. Of that sum, $12.1 billion goes to Sprint shareholders and $8 billion goes to the balance sheet.

- 55 percent of Sprint shares will be exchanged for $7.30 in cash. The rest will become shares of the newfangled Sprint.

- The deal closes in mid-2013.

- Sprint CEO Dan Hesse and other leaders behind the telecom's LTE wireless overhaul remain locked in.

- Softbank will help Sprint roll out LTE and gets access to the U.S. market.

- Softbank Chairman and CEO, Masayoshi Son said his company has had a "v-shaped earnings recovery" and can do the same with Sprint.

- The new version of Sprint will float a convertible bond that translates into common stock at $5.25. This move will dilute existing Sprint shareholders heavily.

Lost in the Softbank and Sprint lovefest is the reality that the wireless carrier still faces a tough time in the U.S. Here's a look at what this deal does---and doesn't do.

What Softbank's investment does...

- Sprint is clearly saved. The company had cash, but also had a lot of debt. It will still have a lot of debt, but a balance sheet that can take a punch. For perspective, Sprint had $21 billion in long-term debt and a market cap of less than $17 billion. Macquarie analyst Kevin Smithen cuts to the chase:

Not a bad outcome for a company many investors told us was going bankrupt as late as March.

- Sprint will be able to consolidate Clearwire, alleviate a spectrum crunch and do it in a way that doesn't require a lot of new debt. Of course, Sprint doesn't have to do anything with Clearwire at the moment. The point is that Sprint will now have the option to consolidate Clearwire. Before Softbank's cash infusion, Sprint didn't have the balance sheet to do a Clearwire deal.

- The Softbank deal also allows Sprint to keep its current executives and network vision in place. Sprint will be able to compete on LTE with the likes of Verizon and AT&T. Softbank CEO Masayoshi Son is basically betting that Sprint can disrupt the mobile market as Softbank Mobile has in Japan. Son has pushed Softbank Mobile to take on NTT Docomo as well as KDDI with some market share success. Judging from the investor call, Son is betting he can speed up the Sprint network and make it faster than rivals.

- Softbank becomes a global wireless player much like Vodafone and Deutsche Telekom via T-Mobile.

- The deal transform's Softbank's business and provides it with more revenue and EBITDA. Couple that bulk with interest rates near zero in Japan and Softbank has a lot of capital to play the mobile game. Indeed, Softbank with Sprint is the No. 3 carrier globally.

What the Sprint-Softbank deal doesn't do...

- For starters, Softbank's cash infusion doesn't really eliminate Sprint's debt. It's not like Sprint deleveraged overnight. That reality will become clear in the years ahead.

- Provide LTE spectrum. Sprint consolidates Clearwire more or less, but it already had access to that.

- Boost Sprint's network immediately. For all of Son's talk about how U.S. networks are too slow, it's unclear how exactly Softbank-Sprint are going to leapfrog LTE. At this point, Sprint is playing LTE catch up.

- Offer any synergy. Softbank can lend expertise and money to Sprint, but there aren't a lot of natural connection points. In many respects, Softbank resembles more of a mobile carrier mutual fund than a cohesive carrier. Softbank and Sprint are on two sides of the world. Jefferies analyst Thomas Seitz pointed out:

In our view, wireless mergers generally generate a large amount of synergies as the merging carriers are able to save on marketing and administrative costs, consolidate networks, and save on tower and equipment costs. Since Softbank does not have any existing U.S. wireless operations, synergies are likely to be modest.

- Enable Sprint to stay independent. Sprint is still going to be squeezed from above and below. AT&T and Verizon lead the U.S. from above and Sprint will still be No. 3. The catch is that Deutsche Telekom orchestrated the T-Mobile-MetroPCS deal. In other words, T-Mobile will be stronger at No. 4 and could breathe down Sprint's neck for years to com. Sprint still could wind up merging with T-Mobile once the LTE rollouts are done.

Earlier: Sprint announces 70 percent stake sell to Japan's Softbank