Is it IT's last chance to lead digital transformation?

A strange thing happened at most companies last year as they were planning their 2015 IT budgets: They largely left out the new resources required for IT to undergo an increasingly much-needed generational change.

Specifically, the change needed today is to shift out of being a relatively stodgy centralized technology support department -- a role long invested primarily in automating and incrementally improving the existing business -- and move into developing sleek and fast-moving new digital lines of business that create growth markets and make-or-break P&L for the organization.

While much has been made of the Chief Digital Officer in leading up the new digital business in many organizations, the challenge has long been that a) the vast bulk of enterprise data, b) expertise in current systems and the business itself, as well as c) existing infrastructure and operations, is typically still owned by the CIO, who often is happy enough to share them, but has other priorities to worry about.

Limited IT Budget, Growing but Tactical Purview

These days CIO priorities are typically business/IT alignment, cybersecurity, "can't ignore" new digital products like new mobile devices, SaaS , and orchestrating the complex ballet of an always growing legacy portfolio. And usually not driving rapid industry-changing digital advances for the business.

Thus the average IT department is in the slow lane when it comes to rethinking the business in digital terms. This is especially true when compared to pure-play digital firms which typically have much higher investment levels, just over double their non-digital peers. (See chart below, IT spending as percent of revenue.)

Unfortunately, as Larry Dignan pointed out last year, the data shows that the average IT department will see an anemic 1% budget increase in 2015, despite more digital change and backlog accumulating than ever before.

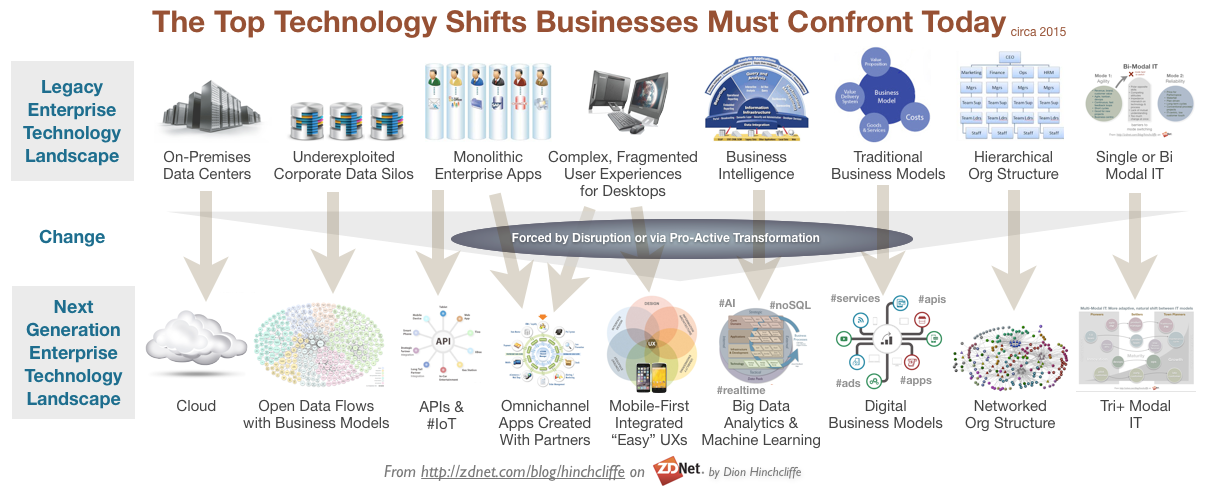

As I pointed out when the "big five" IT changes came down the pike three years ago (mobile, social, cloud, consumerization, and big data), which were seen as an unprecedented series of simultaneous changes at the time -- and in which we are still mostly in the early to mid-point stages of adoption in organizations today -- that the gap between what's achievable and what's needed might become untenable. Combine these in-process changes with limited budget for tackling strategic new capabilities like open APIs, Internet of Things, omnichannel engagement, machine learning, digital business models, rethought digital workplaces, and new models of IT such as bi/tri-modal, and you have a pretty hard to climb mountain of accumulated technical debt.

Related: The New CIO Mandate

The Challenges of "Big Change"

With the success rates of large scale enterprise transformations still hovering around 30% according to HBR, there is not a lot of appetite in most well-managed organizations to bite off big digital initatives that don't almost immediately produce measurable results. Despite this, top performing companies in particular are planning to invest significantly in technology this year, with very little price sensitivity, given the potential upside.

This then paints a pretty clear picture of the priorities and challenges of corporate leaders when it comes to digital transformation: The data shows that large transformation investments are bound to underperform, but our competitors are clearly investing heavily this year, especially at the front of the pack. With the well-known Winner-Takes-All tendency of digital business, it's increasingly hard not to make a move and take the risk, as the inability to win at least second or third place is increasingly outright failure itself.

Yet if you asked most CIOs what their top priority is in 2015 -- and some people certainly have -- the far and away answer (71%) would be surprisingly tactical "to improve applications to better fit business processes."

This is not a prioritized worldview compatible with even the medium-term sustainability of the modern organization. The issue is this: When you look at the major forces shaping the macro business landscape, technology absolutely tops the list, literally reshaping today's list of markets winners and losers, the leaders and the laggards, with apparently inescapable force. To support this, I often quote the respected Technology Review's examination that the lifespan of the top companies today has been dramatically shortened, and continues to be truncated further, by increasingly rapid pace of digital innovation.

So, comparing the top reported priorities of our tech leaders with the increasing urgency of adaptation to today's market environment, combined with budgets that clearly aren't up to the task -- and aren't even in the ballpark with the investment levels of digital firms -- and you have an almost seemingly willful blindness to tackle the combined challenges and opportunities of digital modernization. As long as the company is not faced with imminent ruin, it seems, the apparent risks of attempting digital transformation -- repeated until successful -- makes us look away.

Many of us are familiar with the also-rans that waited until too late, or never clearly got the transformation message of the era: Kodak, Blockbuster, Borders, Nokia, RIM, Sears, the list goes on, even for relatively protected industries like finance and heathcare,

Most Organizations Not In Proactive Digital Stance

So in 2015 it's never been more clear -- and I'm referring to the data now -- that most organizations either a) not currently making a serious investment in digital transition or b) letting investments "on the edge" or with "shadow IT" in the lines of business stand in as placeholder to innovate as an organization, especially in areas like finance and operations.

In addition, many of the organizations I speak with regularly are increasingly well aware that the venture capital model has a 1 success to 10 attempts ratio built right into the business model. That's a lot of failure that traditional enterprises just aren't equipped to deal with. Instead, some organizations are now content with using M&A to back their way into digital innovation by acquiring early successes before they're too large.

Ironically, not innovating yourself directly often keeps you in the game: The most recent available hard data shows that the long-term corporate winners are usually those that carefully use M&A in a steady program over 10 years or more to acquire needed boosts of innovation. In other words, taking risks with other people's portfolio is a viable approach to digital innovation, if done correctly.

This then takes us to an interesting place, where it appears only the bold actors are favored: Digital success -- and ultimately our very survival as enterprises -- requires either being 1) a "top performer" that extensively invests internally in promising technologies likely to boost growth, in the process boosting IT budgets to close the parity gap with digital companies, or 2) using financial acumen, an eye for external innovation, and strategic planning to buy up what you need technologically, when you need it, leveraging other people's investment and risk-taking in the process.

In the end, the middle and bottom of the bell curve of companies in terms of digital investment (either boosting internal IT spend or M&A) -- as well as the cash poor and already poor performers -- are most likely to be squeezed out.

Therefore, when I look at the tall order that companies must face today when it comes to technology shifts (see first diagram above), and I look at the data on where they are in terms of investment today, I see an increasingly closing window when it comes for corporate leaders in building the right capabilities their organizations' require to propel their organizations sustainably into the future.

Of course, it doesn't have to be this way. But creative destruction is arguably the fate of all organizations today. It's just a matter of doing it to yourself, or letting it happen to you. In my opinion, due to accidents of history (resources, capacity, purview) IT is still potentially in the driver seat, but not for much longer, and it will have to adopt a new mindset of risk and innovation to succeed.

Related:

Saying CX is a priority is easy. Following through on it is tough.