Moore's Law may be dying, but there's still plenty of demand for faster chips

It is becoming harder and more expensive to scale chips, and Moore's Law--the engine that drives computing and electronics--seems to be winding down. But the demand for faster, more capable processors that use less power remains driven by everything from luxury sedans to smartwatches. At his eponymous processor conference this week, industry analyst Linley Gwennap talked about these conflicting trends and what they mean for the industry.

The conference traditionally focuses on embedded processors. These chips don't have the same name recognition as the Intel Core processor, but there are many more of them toiling away in everyday devices such as ATMs, networking and communications gear, cars and other vehicles, and of course the Internet of Things. Of the total processor IP market (15.3 billon chips shipped in 2014), mobile is the biggest at 6 billion, but embedded is nearly as large and growing faster, followed by enterprise (including PCs), consumer and flash storage. As these applications grow more complex (and demanding), the industry is shifting from general-purpose processors to highly application-specific processors packing more functions onto a system-on-chip (SoC).

Until recently chipmakers could rely on physical scaling to meet most of these challenges. By jumping to the next node, they got better performance, lower power and more transistors to work with in a given area to add new features. But Moore's Law is running out of steam and Gwennap said the cost per transistor increased at 20nm, and again at 14nm, because of additional lithography steps. "It used to be that everybody moved to the next node because it was cheaper, better and faster, and that was great," he said. "Now it is much more complicated."

These complex SoCs also require knowledge of the intended application, access to lots of intellectual property, and a complete platform including software. Many companies are also choosing to design their own custom cores, in particular on 64-bit ARMv8 because the ecosystem is very familiar to the engineers and programmers that are designing these systems. Examples include AppliedMicro's X-Gene, Cavium's ThunderX, Broadcom's "Vulcan" core, and according to Gwennap, a Marvell custom ARMv8 core. ARM SoCs are increasingly using APIs to offload tasks from the CPU to the GPU, DSP (Digital Signal Processor), or specialized image or vision processing engines that can handle them more efficiently. In some cases, they are using network-on-a-chip (NoC) IP from the likes of Arteris, NetSpeed and Sonics to stitch together all these various blocks.

Only the largest semiconductor companies can tackle all of these challenges, and the result has been a wave consolidation. Intel, the leader in embedded because it leverages the PC hardware and software ecosystem, plans to buy Altera for $16.7 billion. The number two company, Freescale is merging with NXP Semiconductors in a $40 billion deal. Avago, already a player in this space through its LSI deal, is the process of acquiring Broadcom for $37 billion. Other players in this space such as Cavium, AMD, Marvell and AppliedMicro could also be acquisition targets as companies like Qualcomm and Intel, as well as consortiums in China, seek to expand into embedded growth areas. Skyworks also announced plans to acquire PMC-Sierra earlier this week.

Things have gotten especially confusing (and cutthroat) in networking and communications. Gwennap said that as the standards fall into place, data centers and service providers starting to implement NFV (network functions virtualization), which makes it possible to use standard servers in place of proprietary hardware. Intel is moving beyond the control plane, and now has server and networking SoCs that extend into the data plane, the ARM guys are all going after servers and embedded, and speedy network processors are starting to look a lot more like general-purpose processors (EZchip's NPS-400, for example, runs Linux and uses standard programming languages and tools). Service providers are also using smart NICs from Cavium, EZchip/Tilera, Netronome to offload basic tasks from server CPUs and improve the efficiency of their networks. Finally security is a big issue here and it requires specialized processing with a custom ASIC or a security engine integrated in an SoC. At the conference AMD even pitched its APUs with on-die Radeon graphics as a way to accelerate IPsec, a protocol for secure Internet communication.

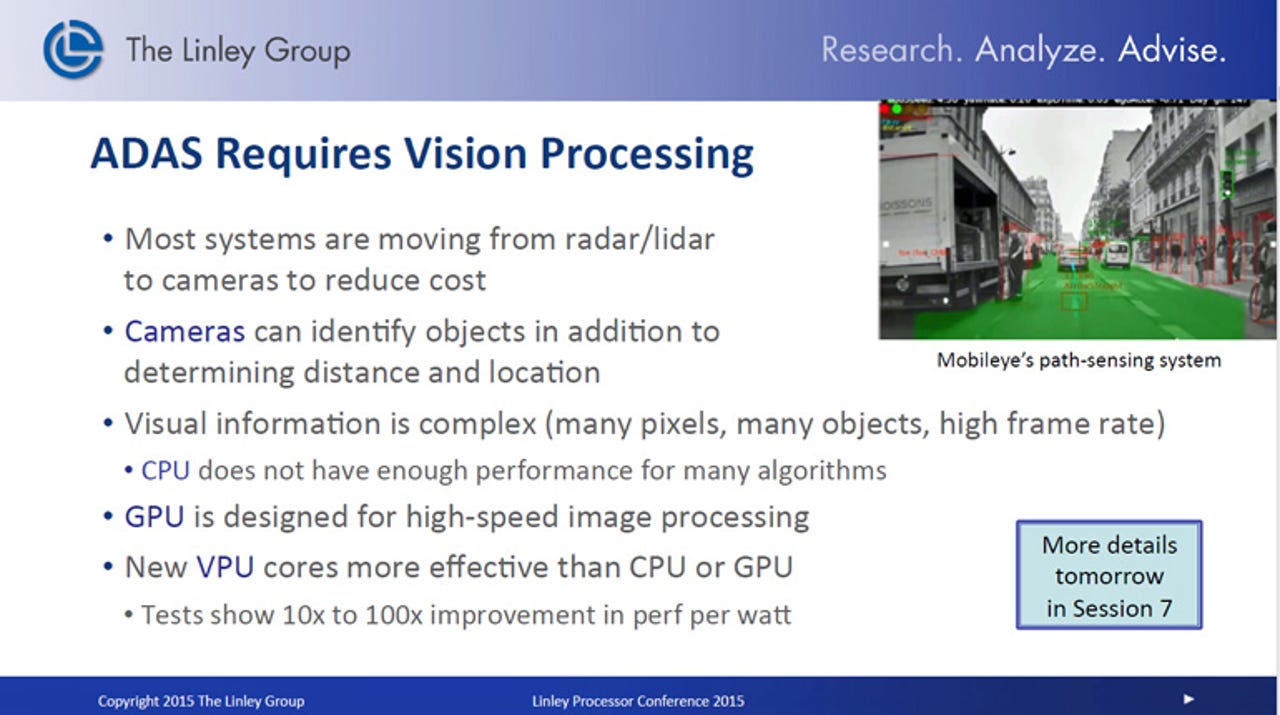

It was interesting to see how another market--automotive--took over this year's conference. The semiconductor industry is clearly counting on it to be the "next big thing." Automotive is already a pretty big market--our cars are packed with microcontrollers that handle everything from the wiper blades to the Engine Control Unit--but more advanced applications such as ADAS (Advanced Driver Assistance Systems) and eventually autonomous vehicles require much more sophisticated technology. ADAS, which includes things like adaptive cruise control, blind spot monitoring, driver monitoring (drowsiness), lane departure and automatic emergency braking, requires either a GPU or a dedicated vision processor. One of the more interesting trends at the conference was the development of advanced vision DSP or processor IP from Cadence/Tensilica, Ceva and Synopsys that can deliver 10x to 100x better performance per watt than a CPU or GPU. These will compete with Mobileye, the market leader, and Nvidia's Drive PX. Eventually we'll get fully autonomous vehicles. These will clearly require a very sophisticated level of processing power. Gwennap also note the progress on self-driving cars and said he expects to see them his the road starting around 2022. Overall automotive semiconductors is a $10 billion per year market and the Linley Group expects it to double over the next decade.

The Internet of Things story is more mixed. Gwennap noted that IoT is really just a new name for embedded systems with an Internet connection. The industrial IoT market is moving quickly. There are already 300 million smart meters deployed and intelligence is being added to everything from vending machines to harvesters. But ultimately industrial IoT is limited, Gwennap said, because "there just aren't that many factories or hospitals that need this technology." The consumer side is different. It has been slower to take off because the products are still relatively expensive, and they don't save consumers a lot of money. The smart home hasn't really happened yet, and while fitness trackers are doing well, smartwatch sales are still small. But as prices come down, and the apps get better, this market will begin to take off and ultimately it will be a bigger opportunity than industrial. The Linley Group has perhaps the most conservative IoT forecast because it only counts new applications and assumes real growth in consumer IoT doesn't begin until 2017. It expects to see 1.9 billion IoT device shipments per year--or roughly the size of the current mobile phone market--by 2020. That's a far cry from Cisco's 50 billion connected devices and objects by 2020.

More coverage of the Linley Processor Conference 2015: