Oracle's second quarter: Cloud offerings, engineered systems at odds

Oracle's second quarter earnings report and ensuing conference call Tuesday will feature a heavy dose of talk about cloud applications and engineered systems. However, there's some evidence that these two product lines are at odds for Oracle customers.

Wall Street is expecting Oracle to report second quarter earnings of 61 cents a share on revenue of $9.03 billion.

The company has a bevy of issues in the second quarter. First, the economy is shaky. Then, Oracle faces competition from the likes of Workday and Salesforce.com. And finally, Oracle's grand plan to grow hardware revenue never panned out. Toss in Oracle's sprawling cloud product line and there's a lot to navigate.

Perhaps the biggest issue for Oracle is navigating two growth strategies at odds with each other. On one hand, Oracle is on the cloud band wagon. Elsewhere, Oracle is trying to sell you souped up boxes to build your own cloud.

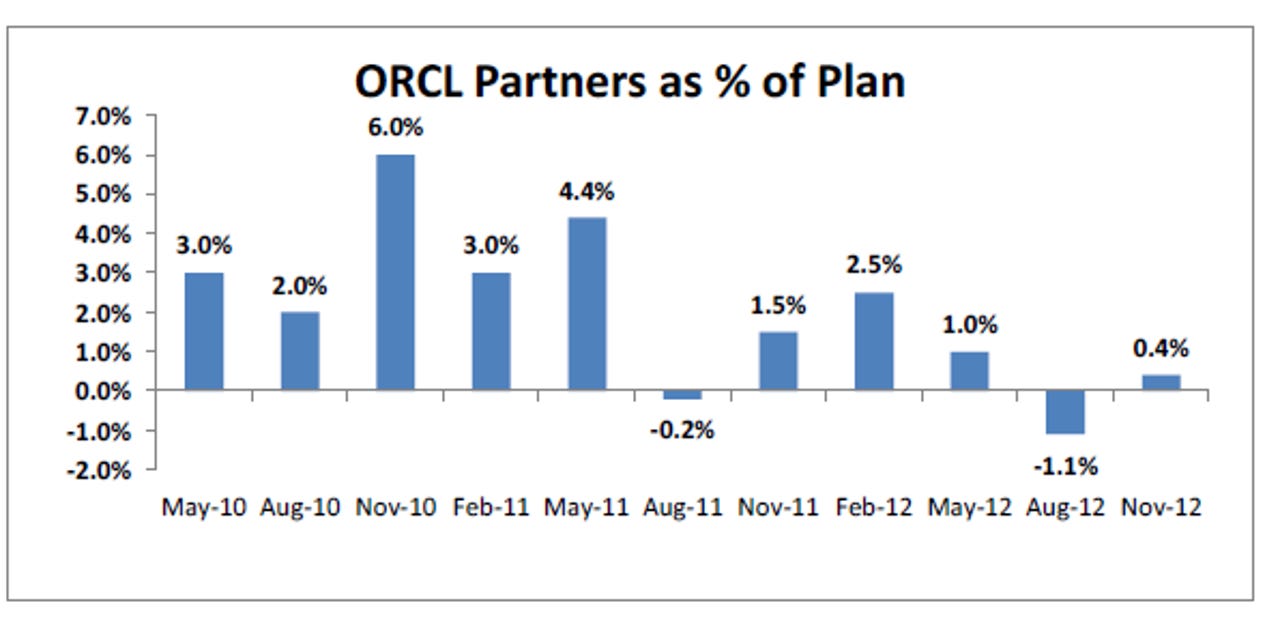

An Oracle partner survey by Piper Jaffray analyst Mark Murphy illustrates the conundrum. Murphy found that Oracle's second quarter was ho-hum, but that reality may qualify as good news. Oracle's growth days, however, may be behind it.

But Murphy's breakdown of partner quotes is worth noting.

On the cloud front, partners said:

Oracle Cloud Offerings are coming in a big way and I feel that is the trend that will rule the market for the next few years.

That upbeat assessment was countered by:

Continued growth of SaaS products, increased integration needs. New competition from open source products like Hadoop.

Clearly, Oracle will have its cloud hands full. But ultimately its cloud offerings may curtail engineered systems growth. Murphy quoted a partner saying:

Clients are split between those seeking Cloud solutions vs. those desiring the purchase of a souped-up box. This makes it a challenge for Oracle's sales force as they need to balance the two strategies.

Indeed, those two products can conflict---not that other tech giants don't have the same issue. Regardless, Oracle will have to navigate those sales conflicts going forward.

For now, analysts say that Oracle's cloud strategy is getting some traction. Evercore analyst Kirk Materne said:

We believe Oracle’s cloud strategy and Fusion apps are starting to gain some traction in the market, and we expect the Taleo and Rightnow acquisitions could provide some buffer to our estimates as Oracle is aggressively pushing these products into new international regions, especially Taleo.

Among other items to note in Oracle's second quarter:

- Analysts generally think Oracle has a low second quarter bar to clear due to worries about the economy.

- Oracle's future depends on the company selling to its installed base. At some point, Oracle's Fusion sales will be closely scrutinized. Oppenheimer analyst Brian Schwartz said:

We think Oracle 's current large deal-driven sales momentum can be sustained long enough for its organically driven product strategy (engineered systems, Fusion apps, database 12C) to successfully re-energize its product portfolio. This should put Oracle in a better position to monetize on its large installed base in 2013 and 2014.

- But the economy is a big wild card. It's unclear whether Oracle can accelerate license growth in a weak economy where IT buyers are increasingly looking toward the cloud to cut costs.