SAP Standard Support price rise: why now?

Yesterday's announcement by SAP that it plans to raise prices for Standard Support by an effective 5.5 percent in July (18 percent to 19 percent represents a 5.5 percent increase in real money), while long anticipated, opens up old wounds that contributed to the demise of former CEO Leo Apotheker just about three years ago to the day.

SAP has tried to sugar coat the pill by saying:

To be able to provide the same level of support in the future, we will change the maintenance rate for new maintenance contracts with SAP Standard Support from 18% to 19%, effective July 15, 2013.

This moderate adjustment does not apply to any existing maintenance contracts for SAP Standard Support closed before July 15, 2013. We also want to be respectful about budgets being planned for 2013. Therefore, we encourage you to take advantage of the opportunity to place purchase orders with SAP Standard Support ahead of this change at the existing 18% rate until July 14, 2013.

SAP threw a sop to customers saying the price rise will not impact BusinessOne customers. My guess is the cost of collection outweighs the revenue likely to be achieved from that source.

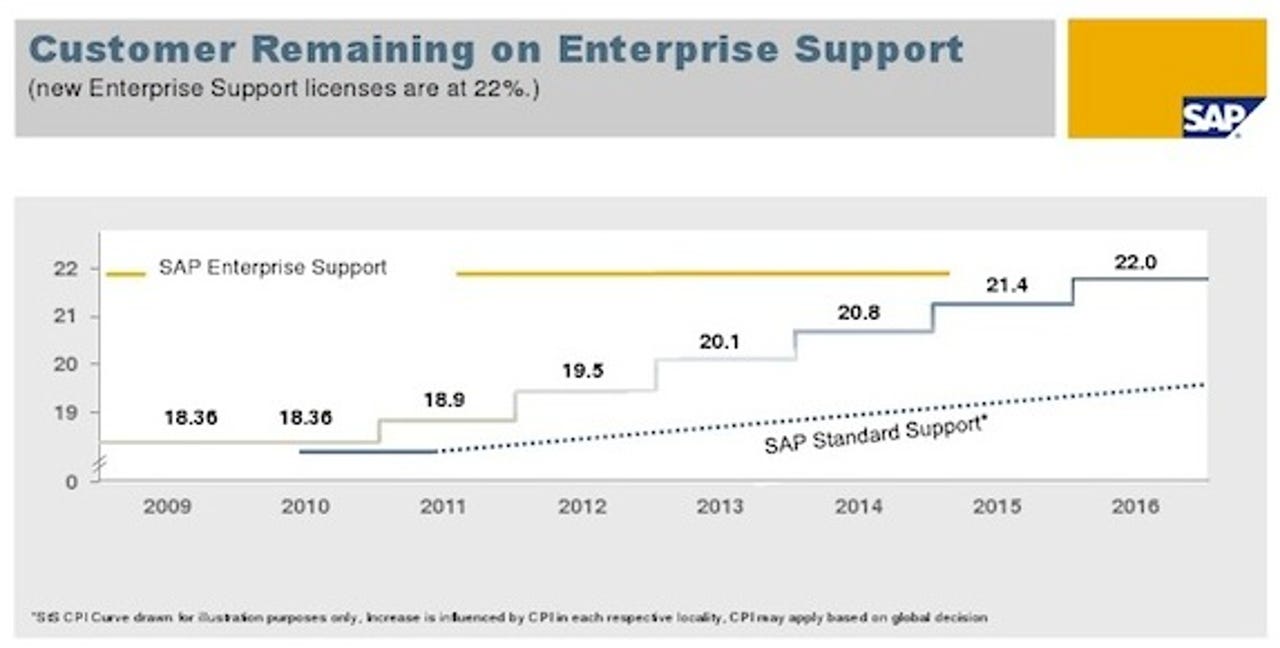

Chris Kanarakus reports SAP has 95 percent of customers on the more expensive Enterprise Support. I find that hard to believe but let's take them at their word for the moment.

Right now, SAP maintenance and support revenue is around the $11 billion mark. If SAP is to be taken at its word then the best case revenue impact adds something around $25-30 million to the top line but likely much lower. In SAP terms that's petty cash. Most of any revenue increment will drop straight through to the bottom line. That is of greater importance as SAP tries to claw back margin it lost in 2012 as a result of acquisition costs, R&D and ramping the sales teams for 2013. The downside is that it opens the door to the third party maintenance providers to come swooping in and make a strong cost saving play.

This from an email sent to me by David Rowe, SVP and CMO, Rimini Street:

Software vendors already enjoy upwards of 90% gross profit margins on maintenance fees, and this latest surprise price increase by SAP is just another example of why more and more licensees - including 69 of the Fortune 500 - have switched to Rimini Street's award-winning support program. We invite every SAP customer to get a proposal from Rimini Street. SAP licensees win either way - by gaining leverage when negotiating annual support pricing, SLAs and service features with SAP or by switching to Rimini Street's premium service with more than 50% annual savings on maintenance costs.

Hardly surprising but then Rimini Street is already looking at forward bookings of $558 million, suggesting that it is having little difficulty in signing customers for periods well in excess of five years. Taken in those terms, my guess is that this move by SAP is designed to lock in 'steady state' customers to the current price as a long term revenue protection measure while it attempts to encourage customers to switch to the Business Suite run on HANA and so re-ignite the core apps sales engine.

Even so, Frank Scavo makes the point that SAP needs to explain:

How have SAP's cost of support increased to justify this increase in my maintenance fees? Normally the cost to support mature products decreases over time, as issues with the program code are resolved. Offshoring of application support and deflection of support activities to SAP's user and partner network also have introduced support efficiencies. Shouldn't SAP be considering a reduction in maintenance fees rather than an increase?

In email, Vinnie Mirchandani confirmed Frank's hyopthesis adding:

Increasing list allows them to discount from a higher starting point but for a customer who pays full it is difficult to justify because SAP has been offshoring support, moving first level queries to be often resolved in SCN, automating help cases, reducing investment in new functionality for old products. Their costs have dropped not increased.

It was only late last Fall that 97 percent of SAP's UK and Ireland user group was asking that SAP allow its customers to park unused licenses for support cost purposes, a move SAP is loathe to consider anytime soon.

Add it all up and you get a powerful cocktail that can only drive animosity between SAP and some customers at a time when a price reduction, however small, would have had a much more positive impact. Put another way, if you pass on cost savings then the chances of selling more product later are vastly improved. This way, SAP only encourages its 'steady state' customers to either begrudgingly remain as they are, switch to a third party maintenance provider or look for a cloud alternative that delivers more cost savings. The worst case scenario would see SAP leak something around $400 million in top line revenue over time.

Dumping the announcement on partners does little to ease the pain. If anything, it makes life more difficult for a partner ecosystem that is seeing no growth in core ERP, is being encouraged to sell HANA and revisit business intelligence on the back of the 'big data' hype but which is getting little from the SuccessFactors team.

Net-net, I see this as a losing proposition and while some colleagues shrug, they forget that customers have long memories and especially about past actions they felt were not in their best interests.

I asked SAP to come back with answers to the following questions by publication time:

- In 2010, the impression was given that Standard Support would flatline, What has changed?

- The reasons given seem nebulous - can we get detail about the improvements noted in the email to partners?

- Are customers expected to sign long term support contracts in order to lock in this price? If so then what are those term agreement periods?

- What percentage of SAP customers are likely to be impacted by this latest change?

- What answer does SAP offer for those who see this as an opportunity to consider 3PM?

At the time of writing, I had not received a reply from the company. If I do receive answers then this post will be updated.

UPDATE: Answers received from SAP:

“What percentage of SAP customers are likely to be impacted by this latest change?”

We don’t report a detailed breakout of support offering segments, but for guidance you can look to our previously communicated adoption rate of Enterprise Support amongst new customers, which is approximately 95%. The change is not effective until July 15, 2013 and does not apply to any existing maintenance contracts for SAP Standard Support closed before July 15, 2013.

POV: SAP is saying 95 percent NEW customers. Soundings indicate that 30 percent are negotiated separately. That still leaves a significant number of customers for whom there is room for potential negotiation. This is especially important to SAP at a time when core app sales are stagnant.

“In 2010, the impression was given that Std Support would flatline, What has changed?”

Our commitment to customer choice and a tiered support offering has not changed. When SAP reintroduced Standard Support we explained to all customers (and integrated in all contracts) that SAP reserves the right to increase installed Base contracts with cost-of-living indices as per respective contract. This has been executed, in conjunction with our customers, for 2012 and 2013. Please remember, Standard Support only changes for new contracts closed at or after July 15, 2013. We assume that the vast majority of our customers will go for purchasing as budgeted at 18% in the first half of the year, which is why we communicated it so early.

POV: This falls in line with the assumptions around revenue protection.

“The reasons given seem nebulous - can we get detail about the improvements noted in the email to partners?”

SAP Standard Support package stays as it is. But within the package, there is ongoing expansion of value, for example a continuous flow of innovation through enhancement Packs while SAP Standard Support is covering a broadening solution portfolio.

POV: I would like to see real world examples of how this is working for customers in the field.

“Are customers expected to sign long term support contracts in order to lock in this price? If so then what are those term agreement periods?”

SAP does not offer price locks beyond the initial period of the contract.

POV: This still leaves open the door for competitive pricing and third party maintenance