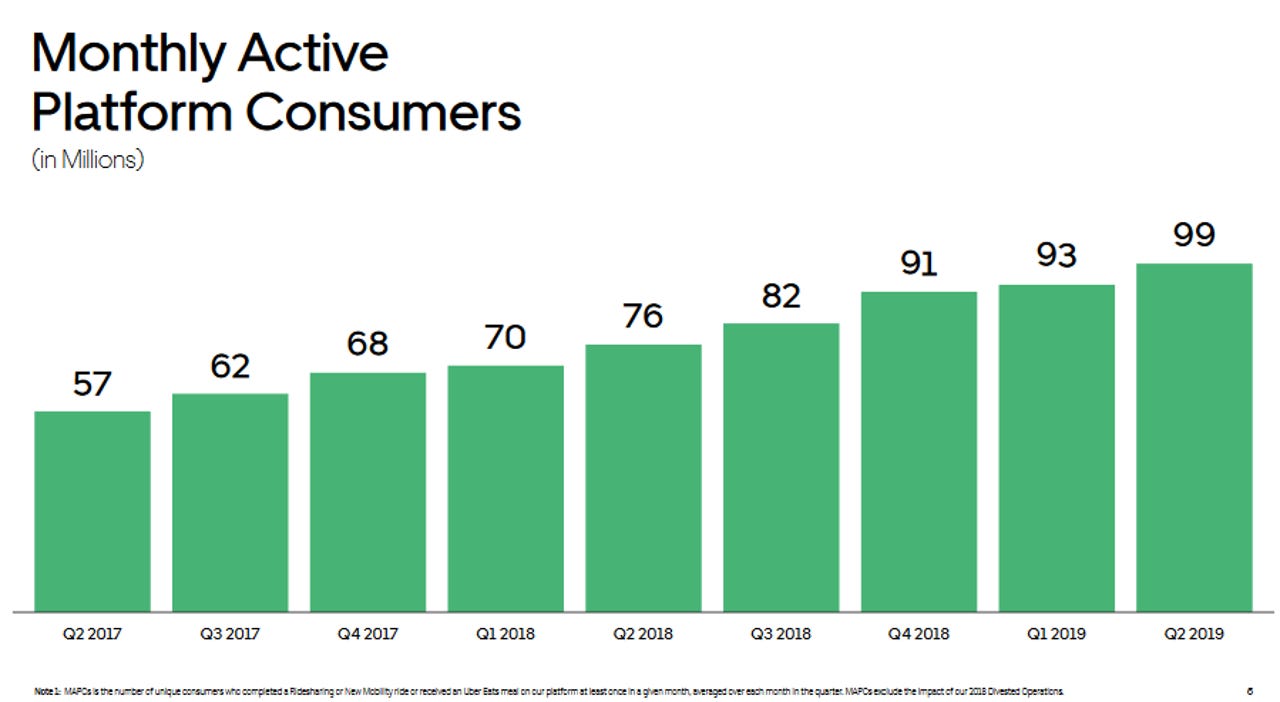

Uber has 99M active consumers on its platform in Q2, but revenue misses

Uber said that it had 99 million active consumers on its platform for Uber Eats and ridesharing, but its revenue fell short of expectations.

The company, which is billing itself as a mobile technology platform that can extend into logistics and other transportation areas, reported a second-quarter net loss of $5.24 billion, or $4.72 a share, on revenue of $3.17 billion, up 14% from a year ago.

Wall Street was looking for revenue of $3.66 billion with a net loss of $3.19 a share.

Uber's net loss includes $3.9 billion in stock-based compensation expenses and $298 million in driver appreciation awards related to its IPO. Uber said it made 1.677 million trips in the quarter, up 35% from a year ago.

Also: Uber vs. Lyft: How the rivals approach cloud, AI, and machine learning

While Uber's revenue primarily is tied to ridesharing the launch of Uber Rewards along with Uber Eats and Uber Freight may diversify sales over time.

The results follow Lyft's better-than-expected earnings report on Wednesday. Lyft indicated that pricing has become more rational and that improved profit margins. Lyft is also focused on ridesharing where Uber has broader ambitions.

By the numbers:

- Uber Eats monthly active platform consumers were up 140% from a year ago.

- Uber Freight saw a 10x year-over-year revenue jump from a year ago from a small base.

- Research and development costs for the six months ended June 30 were $3.47 billion.

- US and Canada were Uber's biggest market by revenue, followed by EMEA and Latin America.

On a conference call, CEO Dara Khosrowshahi addressed Uber's losses and the company's broader strategy. In short, Uber isn't planning to be a money-losing fallen unicorn meme. Some notable quotes from Khosrowshahi include:

On ride sharing pricing:

The competitive environment and our position in the ridesharing space continues to be stable to improve. We will take some of that improvement to continue to lean into our Eats business, where we see plenty of competition and significant capital investment but incredible potential.

While you often have to make trade-offs in life, we believe that we can continue to invest aggressively in growth while driving efficiencies from scale by building great tech to improve effectiveness and from good old-fashioned focus on the bottom line.Customer retention:

We're also ramping up our emphasis on consumer segmentation. Uber Rewards, which you will recall became available to 100% of U.S. rides and Eats consumers in March, has seen great momentum. Enrolled users are about twice as likely to use both rides and Eats than unenrolled users. Uber Rewards is just one part of a broader suite of loyalty products, including Uber Cash, our Uber-branded credit card, and ongoing experimentation with subscription products in rides and Eats.

Uber Eats:

We launched several Eats product features during the quarter including pilots, the test subscription, pricing strategies with our most engaged users. We continue to work on improving restaurant onboarding efficiency by reducing friction including point-of-sale integrations through partnerships such as Olo and custom integration via our own APIs. And lastly, we enabled even more ways for restaurants to engage Eats customers through new options like dine-in, pick-up and the ability to use their own delivery personnel.

Profits:

I think that we can make the trade-offs where we can scale expenses and/or get far more efficient in our marketing and incentive spend while

improving the bottom line of the company. And listen, we're very confident that this company at maturity can be cash flow positive, and the team is focused on being able to drive big-time growth at the top line while getting more efficient on all parts of the business.

I think that there's the meme around, which is can Uber ever be profitable. I've certainly heard that meme along with others. And I'll tell you, we have a business in the rides area that has a 20-plus percent take rate, which is a very, very strong take rate. And a business at scale the way we are a global business at scale but has network effects with a 20-plus percent take rate I believe has the potential and if we execute should turn out to be a spectacular business long term.