Cisco reports solid product order growth in Q3, supply chain challenges

Cisco on Wednesday published third-quarter financial results slightly above expectations with growth across categories. The company reported 10% year-over-year total product order growth, representing the strongest demand in nearly a decade.

At the same time, supply chain challenges are impacting Cisco's expectations for this quarter's adjusted gross margins.

"We've locked in both supply and pricing with some of the key component providers that we've got going ahead, that's what you see built into the margin guide," CFO Scott Herren said on a Wednesday conference call. "And I think the supply chain issues will stay with us at least through the end of this calendar year."

CEO Chuck Robbins added, "If we come to the conclusion that any of these cost increases... are going to be more sustained, then we will look at strategic price increases where we have to. That work is already underway. There are already some decisions that we've made... It's a pretty dynamic situation."

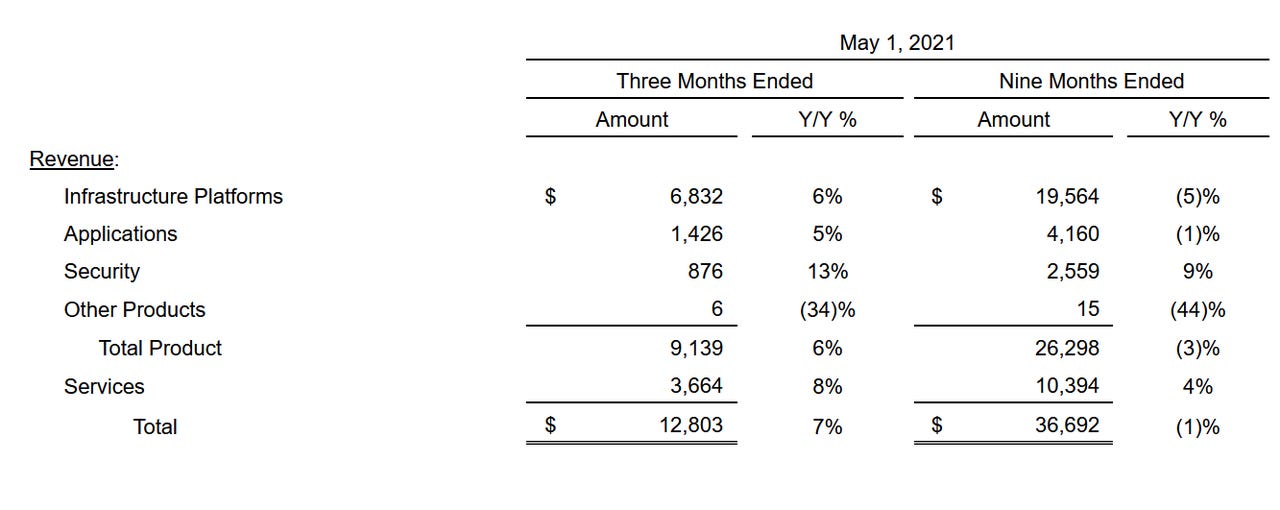

Cisco's Q3 non-GAAP earnings per share came to 83 cents on revenue of $12.8 billion up 7% year-over-year.

Wall Street was expecting earnings of 82 cents per share on revenue of $12.56 billion.

Overall, product revenue was up 6% year-over-year, totaling $9.14 billion. Within that category, security revenue was up 13% to $876 million. Revenue from infrastructure platforms 6% to $6.8 billion, while applications revenue was up 5% to $1.4 billion. Revenue from "other products" declined 34% to $6 million.

Service revenue was up 8% year-over-year, reaching $3.66 billion.

"Cisco had a great quarter with strong demand across the business," Robbins said in a statement. "We are confident in our strategy and our ability to lead the next phase of the recovery as our customers accelerate their adoption of hybrid work, digital transformation, cloud, and continued strong uptake of our subscription-based offerings."

Deferred revenue in Q3 was $$20.9 billion, up 12% in total, with deferred product revenue up 20%. Deferred service revenue was up 7%.

The remaining Performance Obligations came to $28.1 billion at the end of Q3, up 10%.

For the fourth quarter, Cisco expects revenue growth of 6% to 8% year-over-year. It expects a non-GAAP gross margin rate of 64% to 65% and a non-GAAP operating margin rate of 32% to 33%.