How SAP's partner ecosystem is built for long-term growth

How is SAP's partner ecosystem poised to propel the company towards vital future growth in the cloud? Will this ecosystem earn the enterprise IT leader its sought after slice of the global digital economy, whose app economy alone will be $120B this year? These were the key questions at a recent strategic SAP Partner forum I attended in New York City.

The upshot: While the SAP Partner story overall is strong for the firm, there remains critial work to do to prepare for the future and fully realize its potential to achieve the company's strategic goals.

SAP's Success Through Partners

The German software giant is well known for providing some of the most mature and sophisticated enterprise solutions in the world. As the saying goes, there are average industry solutions that can't be counted on to work in practically every market, industry, and operating environment. And then there's SAP. It's a reputation that the company has burnished at every opportunity.

This expectation cuts both ways however: While it separates the also-rans from the top-tier and allows premium pricing, it also provides real delivery and customer success challenges in making sure the more advanced capabilities of SAP's platforms are actually differentiating results in reality to provide additional business value for the customer.

Enter SAP's partner ecosystem, which often provides the last mile of success, by having a large global set of delivery partners that have 1) a nuanced understanding of the history and needs of local customers and SAP products both, plus the ability to bring them together effectively, 2) built additional unique capabilities and solutions on top of SAP's many platforms, and 3) integrated all of these elements together, along with 3rd party legacy IT systems, into workable enterprise IT portfolios.

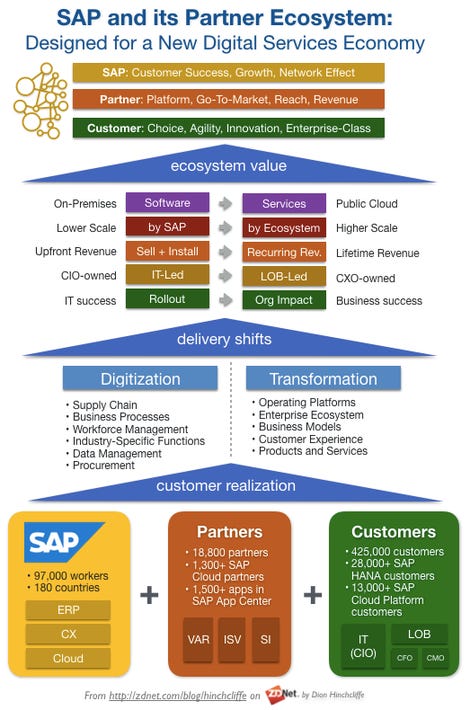

In other words, it's the classic trinity of VARs, ISVs, and SIs that make so many enterprise software vendors successful on the ground, and especially so in SAP's case. In fact, today one key measure of real success for an enterprise software vendor is how many such partner organizations can be brought into its orbit. By this measure SAP is still a bit behind organizations like Microsoft, which has over 68,000 cloud partners albeit more SMBs.

State of SAP's Partner Economy and Ecosystem

As a result of its domain complexity, the considerable size of the ERP market, and SAP's dominance of supply chain IT in particular -- though the company is fast moving into many adjacent markets -- SAP's partner economy is vast, with over 18,800 partners as of late January. The total value of this partner application economy was recently pegged at $130 billion in net new yearly revenue, and slated to double over the next five years. Thus, the company's partnership ecosystem stands both as an engine of success as well as growth for the company.

With so much staked on its success, SAP recently gathered analysts and thought leaders together at the SAP Business Partner Forum in New York to showcase success stories and the current state of its partner ecosystem.

Kicked off up by Meaghan Sullivan, head of general business and global channels marketing at SAP, she underscored how the company is committed to building a true "ecosystem of the future" to achieve its vision for the Intelligent Enterprise, a roadmap the company has developed for strategically wielding enterprise data that is designed to outmaneuver competitors with smarter products and services. It's a sophisticated model that they are current touring around the country to explain to the market better. Both comprehensive and deep, the Intelligent Enterprise is inclusive of supply chain and (most recently) customer experience, as well procurement and workforce management. It also includes a growing number of industry verticals with its SAP Leonardo offering.

Perhaps the most insightful comment of the day came from Diane Fanelli, SVP and GM of SAP's Global Platform Channels, who noted that when it comes to the IT solutions of tomorrow, "the future is small, simple applications that snap into existing landscapes. You go shopping for them on your phone. That trend will continue in the enterprise, as they become more comfortable with this kind of [informal] digital acquisition."

Translation: Like Salesforce has attempted with some success with AppExchange, SAP is building and growing rapidly with its SAP App Center a delivery channel for partners that is more consumerized, on-demand, and ready to digitally expand reach for partners, while driving lower barrier acquisition and sales for both SAP and its partners. Though long-predicted, especially by yours truly, enterprise app stores has been some time in coming. SAP is clearly determined to build App Center out as a next-generation channel and make it successful. The early numbers seem to bear this out: Growth has been rapid given its launch only 18 months ago, with over 1,500 enterprise apps from SAP and its partners now resident in the App Center.

Which brings up a recurring point and one of the areas where SAP can most improve its PartnerEdge program, though it's a famously tough balancing act all enterprise vendors must deal with: With so many partners vying for business, a software vendor will tend to favor its most tried and true partners, especially large ones that can handle plenty of project capacity, and SAP is no exception. While SAP clearly was aware of this perception, as it highlighted smaller players like Blue Marble and Nimbl, the high profile presence of Deloitte underscored the big ecosystem players that traditionally tend to dominate partner activity.

Takeaways for the future success of SAP's partner economy

From this, here's my analysis of the overall takeaways and recommendations for SAP that will help them achieve their goals of doubling the performance of their partner economy through 2024:

- Continue to democratize the partner ecosystem. The App Center is a terrific start, but it's still at an early adoption phase, though eventually it will be a channel for a significant percentage of partner solutions as SAP customers more fully adopt the cloud. However, the broader partner ecosystem, while considered perhaps too large for SAP to service well by some, needs more pro-active governance to equalize access and accelerate its run rate. The U.S. federal government has famously done this with set asides for certain key segments to keep its constituents happy. This model has real potential for SAP to ensure a sense of fairness and equity with its partners. Dimensions for such set asides could include industries, geographies, and solution domains, making them more fine grained if necessary to let smaller partners stand out.

- Encourage streamlining and acceleration of the rest of partner delivery. While digital channels are the long-term future of much of SAP partner solution delivery, real scale for this type of solution acquisition is 3-5 years away. In the meantime, there's a great deal of work that can also be done to productize, template, and automate existing partner offerings to cut delivery time and cost, although likely at the expense of margin in return for speed and scale of customer growth. While Deloitte's SAP CTO Darwin Deano stressed they are working on automating delivery across their 20,000 staff members, they admit it's slow going. To achieve this, SAP will need a few poster children partners that can demonstrate such acceleration means more client projects can be handled at the same time with higher success rates and more revenue.

- Push the pendulum for cloud through the partner ecosystem. Many of the strongest aspects of the future state of SAP's partner ecosystem comes from customers shifting to the public cloud. This ranges from digital delivery of partner solutions through App Center to making its own solutions easier to provide to customers. An SAP Cloud Platform migration kit that helps partners quickly move their on-prem applications into fully productized customer-ready partner offerings would go a long way towards achieving this goal. SAP's is clearly staking its future on the growth of its cloud platform in so many ways. Making it easier for all of its nearly 20,000 partners to move themselves and their customers to the cloud is just smart, and only requires a single point, though sustained investment.

These days enterprise vendors realize they have almost no chance to win in the cloud without a large number of partners to help spread out the scale and cost of innovation, customer acquisition, delivery capacity, client knowledge, support, and much more. This has long been the case when it comes to consumer digital platforms like operating systems and mobile devices, the enterprise software space is finally reaching the tipping point when it's not enterprise vendor vs. vendor but ecosystem vs. ecosystem.

In this way, all enterprise software vendors have the same top digital transformation issue that their customers have: How to achieve ecosystem growth successfully and sustainably at scale, simultaneously. In my view, SAP has succeeded in building one of the largest and most successful enterprise partner ecosystems to support its direct sales channel. Now the challenge will be to transition its sales model for both SAP's offering and its partners' to new cloud delivery channels, from pre-sales and solution acquisition to consulting and delivery. This will have many challenges, especially cultural, as the sales organization can't seem to be threatened. This risks slowing down the transition to become a fast and agile cloud player. In my analysis, SAP certainly has the ability to execute here, the only question remains how well it will be done.

Additional Reading