Wall Street skittish on growing threat to IBM's SaaS, cloud

IBM was downgraded on Monday amid warning bells that the computing giant is struggling to garner growth in the cloud and Software-as-a-Service (SaaS) field.

According to Barclays Capital analyst Ben Reitzes in a note to analysts, the mainframe "catalyst" is over, leaving IBM's traditional server business in trouble. But, the positive benefits from analytics, which the company is expanding into, will be offset by "secular" shifts to the cloud and SaaS.

Reitzes said this shift "seem[s] to adversely impact all of IBM's segments in some way."

As a result, Barclays is lowering its price estimate down 12 percent down from $215 to $190.

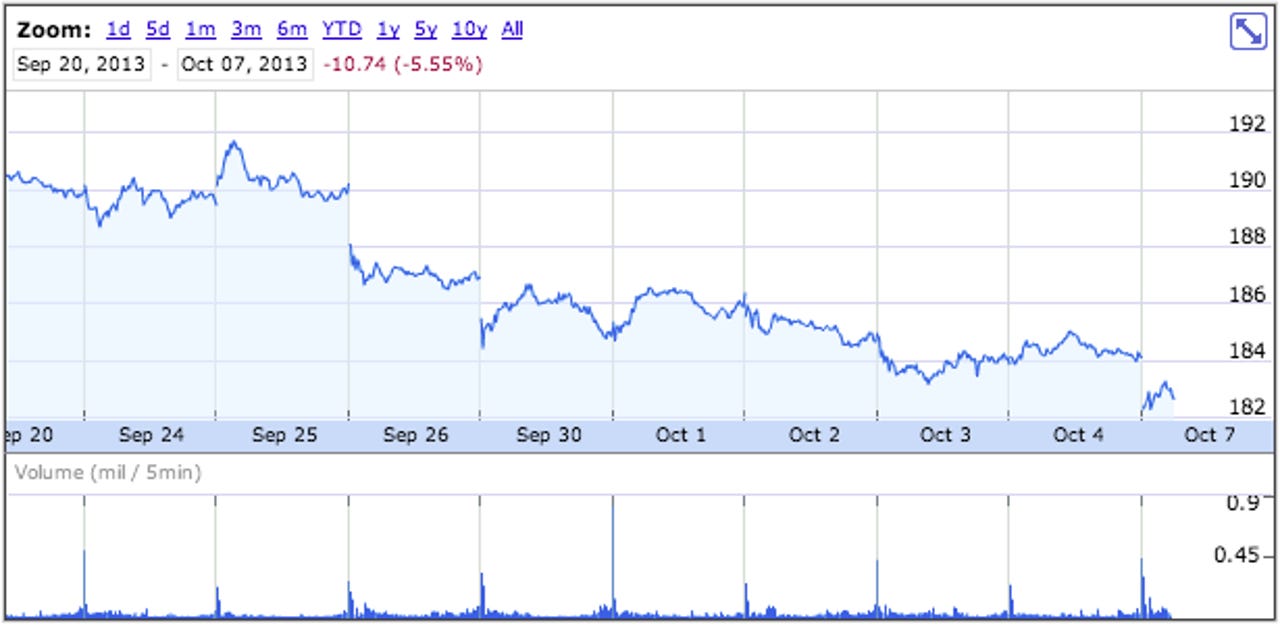

Shares in IBM have been tumbling since the start of this year. Though it recovered on the most part from an 11 percent drop in April from $212 to $187 per share, the company's stock has taken a slow and prolonged battering since.

"It is increasingly clear to us that investors will evaluate IBM on cash flow more than earnings until revenue starts to grow meaningfully," Reitzes wrote. It follows surveys conducted by the bank that suggests the "disruptive impact of cloud and SaaS" have only just begun, and will likely see a shake-up of the entire industry in the coming year.

A few pointers from the note:

- The bank sees "downside[s]" in IBM's hardware business, which made up almost one-fifth of the company's sales in 2012. At its latest fiscal second quarter earnings, hardware sales were down 3 percent on the same quarter a year ago.

- IBM's emerging market efforts are struggling, cited as a "weakness," particularly in regards to weak currencies in some regions. OEM sales were down 24 percent at its fiscal second quarter earnings, and only grew 12 percent in the emerging BRIC nations, consisting of Brazil, Russia, India, and China.

- The company's software division, which recently saw strong growth, is slowing. Barclays is concerned about the acceleration of SaaS deployments — or lack of — by large enterprises. The bank called IBM's own cloud services as "still in their infancy, really."

- And finally, IBM has an greater need to acquire in high-growth areas, particularly in high-growth areas, such as software and cloud. In the past few months alone, Big Blue acquired mobile offers and messaging firm Xtify (and spent more than $3.5 billion on smart commerce related acquisitions since 2010). It also bought analytics firm The Now Factory earlier this month, and virtualization management software maker CSL International for an unknown sum; while shedding its customer care unit to Synnex for half-a-billion dollars.

Barclays' bottom line: "We are more concerned about all our names in “old tech” and believe that IBM’s shares may remain range bound."