WWDC 2017: Can Apple's P2P payments push challenge Venmo?

WWDC 201

Apple officially entered the person-to-person (P2P) payments fray on Monday with the upcoming release of iOS 11, which will bring Apple Pay to iMessage.

On the surface, the effort looks like a direct assault on services like PayPal, PayPal-owned Venmo, and Square. But details are scant as to how the service will operate, whether it will provide any real convenience to mobile-paying consumers or serve as the next big use case for Apple Pay.

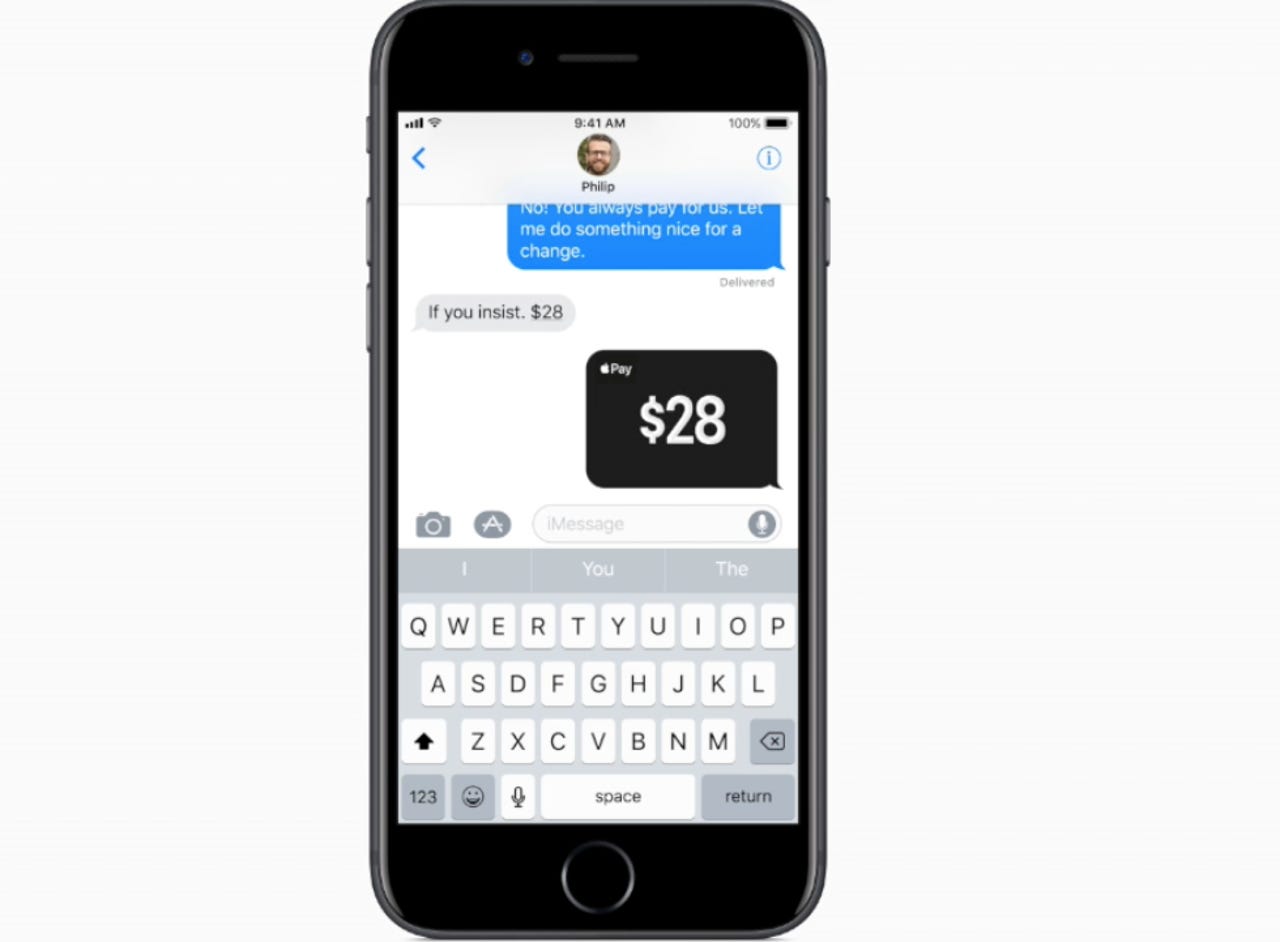

As Apple's senior VP of software Craig Federighi explained during the WWDC keynote, Apple Pay's P2P functionality will allow people to send and receive money from anyone in the default Messages app who is also running iOS 11. It's integrated with Messages as an iMessage app, and money is sent and received right in the text transcript.

Upon setup, users have to add a debit or credit card to Apple's Wallet app to serve as a funding source. When users get paid, they receive the money in something called an Apple Pay Cash account, where the funds can be used to pay someone else, make purchases, or transferred to a bank account. It's here that the utility of P2P Apple Pay comes into question.

"The details here seem to indicate a system that requires users to access a prepaid account -- even if they have already added a payment card to their Apple Pay wallet -- and then only send and receive money to other iOS 11 users," said James Wester, research director of worldwide payment strategies at IDC.

"That really limits the utility of the system and requires a user to manage yet one more account instead of eliminating accounts. So I don't think it's the Venmo-killing app that was expected."

On the other hand, the perceived limitations of the service -- primarily the prepaid account requirement -- could actually make P2P Apple Pay appeal to younger users and those who lack traditional financial accounts.

Still, it remains to be seen how consumers take to the service and whether Apple can take a bite out of the P2P payments market, which Forrester Research estimates will reach $17 billion in transaction volume by 2019.

Venmo, the undisputed leader in the P2P payments space, has been growing at a rapid clip. In the first quarter of 2017, Venmo processed $6.8 billion in total payment volume, more than double its volume versus the same quarter a year ago.

Apple's ultimate advantage could come via its commerce services push, bolstered by a Maps update coming in iOS 11 that will include indoor location services for malls and airports. What's more, Apple is bringing QR code and expanded near-field communication (NFC) support to iOS 11, broadening its retail and commerce-related capabilities even further.

QR codes aren't widely used here in the US like they are in other parts of the world, which probably explains why Apple hasn't bothered to provide native support for the technology. But iOS 11 will bring QR code support to the native camera app, giving users the ability to scan codes in stores or on product packaging without using a third-party app.

As for the expanded NFC support, iOS 11 will enable the iPhone 7 and newer devices to read NFC tags just like Android. This opens up a number a consumer use cases, particularly in the areas of IoT and retail.

As explained by ZDNet Editor-in-Chief Larry Dignan in his WWDC analysis: "You can see the connective tissue here as Apple profits from the handoff from Apple Pay to internal maps to closing sales and collecting fees."

Related stories: