CommBank App 4.0 boasts location-based tracking and tax return notifications

The Commonwealth Bank of Australia (CBA) has launched its new banking app, an upgrade to the platform that was first released in 2013.

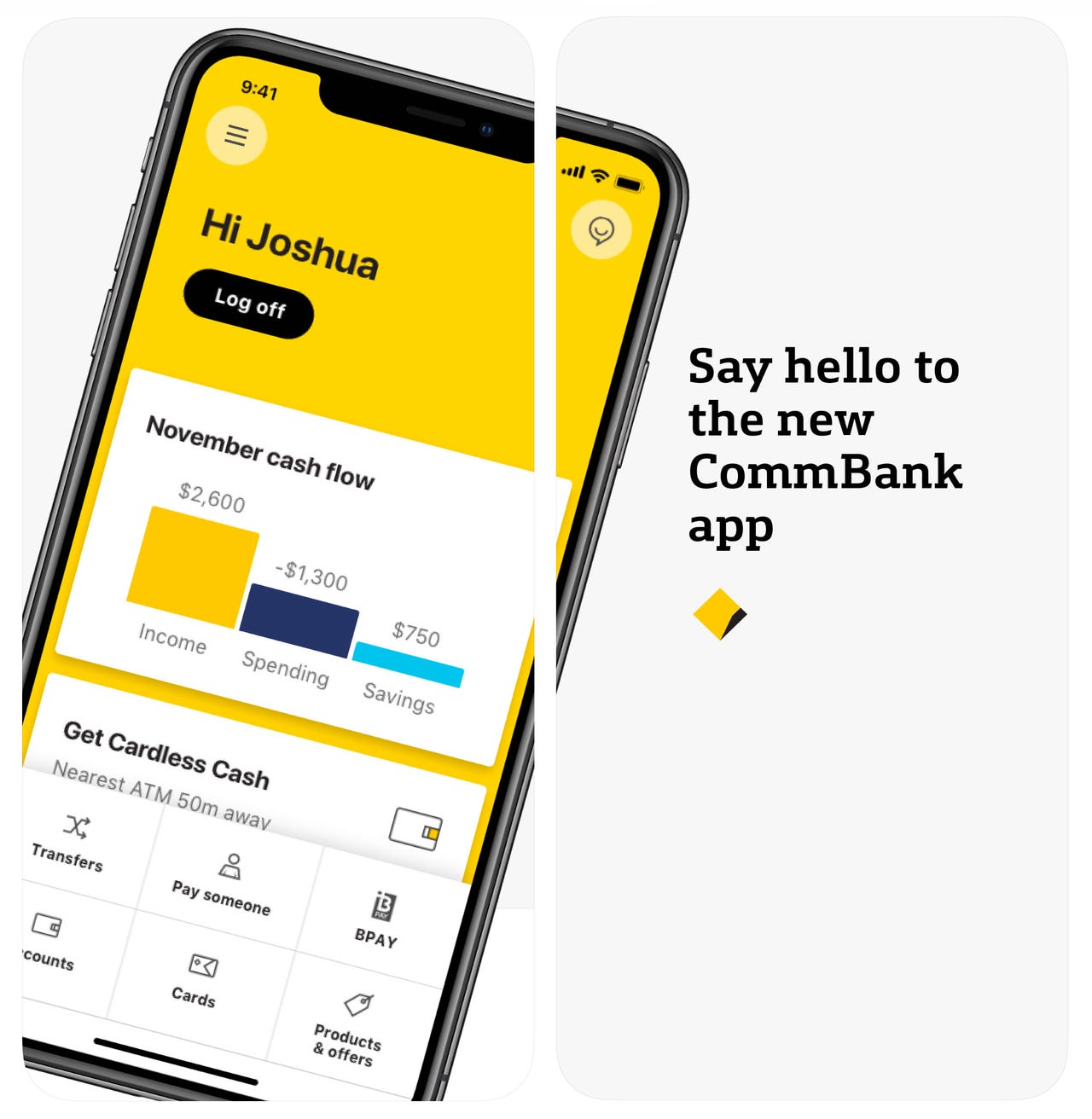

The new app is touted by the bank as offering greater personalisation, tailored specifically to the individual needs of each customer, with personal cash flow management and smart alerts all aimed at keeping more money in customers' wallets.

Speaking with media at the launch of CommBank App 4.0, CBA chief digital officer Pete Steel said the app update comes after the bank decided it could bring all of its technology and digital capability in data and artificial intelligence (AI) to "really solve problems for customers".

The bank boasts that 7 million customers are active on digital channels -- a staggering amount, Steel said, when it converts to being about a third of the adult population in Australia. He also said 5.6 million people have been actively using its 3.0 mobile app.

"The new app, it's a fresh new look and feel -- it's quite unbank-like," Steel said. "Combining functionality and the power of AI and data to bring things to customers' attention quicker, better than ever before. It's a revolutionary technology stack for us as well."

See also: CommBank to launch new machine learning-backed banking app

Steel said the bank has three "relentless priorities" with the new app: Simple, smart, and secure.

Simplicity, Steel said, is making it feel like the app belongs to that specific customer.

"It's targeted, it's personalised, and it's customised for you by you. Customisable like an iPhone and personalised like Netflix recommendations," he said.

He said from research conducted by the bank, it found that one in four Australians struggle to meet their financial commitments and can't really handle the shock of an expected expense.

"One of our philosophical beliefs is helping customers save, helping them learn how to save. So we've been working with Harvard University, on experiments, how to make it a really simple, inclusive experience, set goals, governed by experiences and engaging you on your spending to save for those goals," Steel explained.

"This is our big shift from transactional banking."

An example of how CBA has made the app simpler to use is that it will notify a customer when a direct debit or subscription payment increases, or if a bill has been paid twice. It can also provide advice on what to do with a tax return.

"One example where we've reached beyond the remit of a traditional bank is tax refunds ... hopefully you're not going to spend it on the latest designer handbag or set of golf clubs, we encourage customers to think about that [the refund] might be coming up, but also when it hits their account, a real time alert to say, hey, we suggest -- it's always the customer's decision -- but we suggest you think about paying off some of that debt that you've got, or invest in it for a rainy day," Steel said.

Pointing to the Capital One breach, Steel said CBA has been making large progress both in making the bank safe, but also through helping customers manage their security.

"Financial services are trusted, we need to keep up that trusted relationship. Over AU$490 million are lost each year -- in what we can track -- for fraud and scams. Probably the undeclared number is closer to several billion," Steel said.

"In a world first we are alerting customers in the app to suspicious transactions."

He said in the case of a definite fraudulent transaction, the bank will block it straight away, but if it isn't 100% sure, it will alert the user and direct them to the app to have the issue sorted out.

"For us, this is wonderful because it puts customers in control, helps them help us learn -- and it's almost like crowdsourcing some of the fraudulent merchants out there, so we can spot them quicker," he said.

Steel told ZDNet that the new app also comes with location-based security.

"There are a couple of examples where we're pushing the boat out, one is location-based security," Steel said.

"We allow, on an opt-in basis, customers to enable location-based security on their phone. So we see a transaction coming out of Hong Kong, but we know through the customer's phone they're in Melbourne or Sydney straight away that gives us an opportunity to spot a discrepancy, and log it straight away."

"It's definitely opt-in, so we have very clear privacy policies and transparency from a customer point of view," he told ZDNet. "It'll be something that customers can choose to turn on to let us help track their phone to keep them safe."

See also: NAB admits it shared personal info on 13,000 customers with two external parties

Steel said the bank has also been partnering with third parties to tackle malware.

"We're looking for problems on the customers phone to help them keep their banking safe," he said.

"We also allow customers to set payment limits -- this is where you'll start to see a lot of privacy and security settings come to life."

Perhaps coming in app version 5.0 is biometrics functionality, with Steel telling ZDNetthat while the yellow bank hasn't committed to any date yet, its future biometrics capability is expected to be used in conjunction with government data sources. He said biometrics are already present in certain critical, high-value processes to identify customers.

"The sophistication of financial crimes or criminals is getting higher and higher ... so we've been working with government, authorities, and the rest of the industry on how we use capabilities like biometrics to help make sure we know who we're talking to -- and we're learning as an industry about some of the criminals and perpetrators," he added.

RELATED COVERAGE

- CBA slapped with a court-enforceable undertaking after loss of data on 20m customers

- They said it couldn't be done: Commonwealth Bank gives in to Apple Pay

- Datacentre issue to blame for Commonwealth Bank outage

- Commonwealth Bank hires new execs, touting digital and cultural transformation

- Commonwealth Bank and Austrac reach AU$700m agreement over anti-money laundering breaches

- CommBank to launch new machine learning-backed banking app